Houselungo 10 October 21

A lungo length look at this week's housing market news

Will high wages and high skills mean high house prices?

The puzzling property problem

In his conference speech this week, Boris Johnson said that we are moving towards a high wage high skill economy, but will this also mean high house prices? And if it does, how will higher house prices impact the Government’s desire to solve the national productivity puzzle by fixing the broken housing market?

House prices and wages

The majority of home purchases in the UK are part-financed with a mortgage. Mortgage capacity is directly linked to the borrower’s earnings. In our view, borrowers tend to borrow towards the top end of their mortgage capacity. Higher wages will, therefore, feed into higher mortgage capacity, which, in turn, will put upward pressure on house prices.

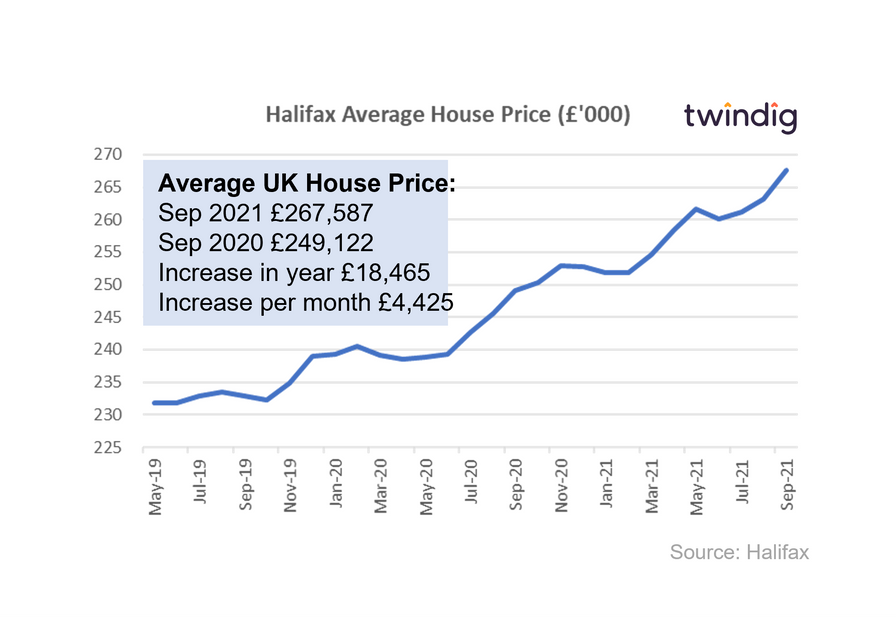

House prices reach record highs in September

The Halifax published their house price index for September on Thursday

What they said

Another record high for UK house prices

Average UK house prices £267,587

Annual house price inflation 7.4% or £18,465

Twindig take

UK house prices rose to their highest ever level in September 2021 according to the latest data from the Halifax. House prices rose by £4,425 in September to £267,587 as the Stamp Duty Holiday drew to a close.

The UK might not yet be a high wage, high skill economy but it is certainly a high house price one.

Whilst the Stamp Duty Holiday may have been a catalyst for house price growth, it does not explain the scale of the increase, house prices rose by almost £25,000 during the holiday against an average saving of £3,379. Homebuyers were made worse off not better off by the stamp duty holiday.

The unaffordability of London housing

For many aspiring first-time buyers, London housing is unaffordable, however, neither house prices nor the pandemic has led to an exodus of those aged 25-45 years currently living in London. It seems that for many, the call of the city is louder than that of the country

More than six in ten (63%) London renters believe owning a home would improve their quality of life, yet just two in ten (22%) are currently able to save money for a deposit, according to research from affordable housing developer Pocket Living, who surveyed more than 1,000 25-45 year-olds during August 2021.

Surprisingly, building more affordable homes may not be the answer, but there is a way to make homes more affordable.

Unaffordable London Housing

Pocket Living found that almost three out of four renters in London (73%) wanted to own their own homes. However, high London house prices were cited as the biggest barrier to homeownership for more than half of London renters (51%), followed by the unaffordability of a mortgage (30%) and more than one in four (27%) saying they are struggling to save a big enough deposit.

Almost two thirds (62%) agreed with the statement:

‘I really don’t want to move outside London to afford a home because I would have to sacrifice too much to do so’

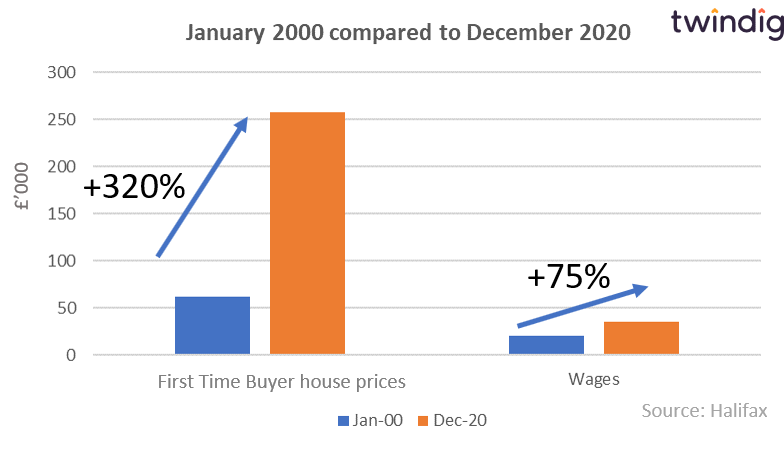

From a £20,000 to a £130,000 deposit

According to the Halifax, at the start of the millennium a typical professional couple needed to raise a £20,000 deposit to buy a home in London, However, 21 years later, in February 2021, the deposit requirement had risen to £132,685.

The half a million-pound average London home

Pocket Living found that the average price paid for a first home was £490,000, more than 12 times the average £40,000 income of the London first time buyer, implying that even with a 10% deposit a London first time buyer would need to borrow more than ten times their income to secure their first home. The lending multiple puts the London housing crisis into context because lenders have to ration the amount of lending they do which is more than 4.5x income, which for many, effectively slams shut the door of homeownership.

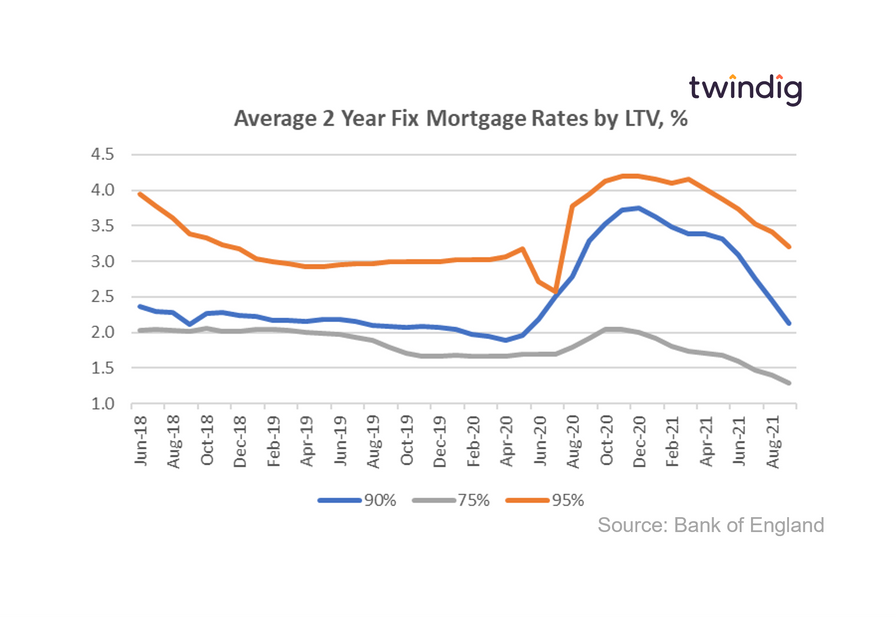

Mortgage rates fall as house prices reach record highs

As house prices reached new record highs in September it will come as a welcome relief that mortgage rates continue to fall. Falling mortgage rates are obviously good news for those with mortgages, but we can also take comfort for what they tell us about the health of the wider UK housing market.

Mortgage rates are set by the mortgage lenders and falling mortgage rates imply that they are feeling more upbeat about the outlook for UK house prices. The risk of lending is falling, which means the lenders are less worried than they were about falling house prices on a two-year view.

Mortgage rates for 75% LTV mortgages

At 1.20% mortgage rates for 75% LTV mortgages are now lower than they were before the start of the COVID-19 pandemic, around 15% lower. For those with equity in their homes mortgage credit is cheap. Welcome news in an environment where energy, fuel and food prices are rising.

Mortgage rates for 90% LTV mortgages

As the LTV rises so does the mortgage rate, the higher the LTV the more risk there is for the lender (smaller house price falls will lead to a loss for the mortgage lender). However, the mortgage rates for 90% LTV mortgage have been falling dramatically over the course of 2021 and they are now only 5% above their pre-pandemic levels

Mortgage rates for 95% LTV mortgages

The mortgage rates for 95% LTV mortgages are also falling and at 3.21% are 24% below their December 2020 highs of 4.2%, and only 6% ahead of their pre-pandemic levels.

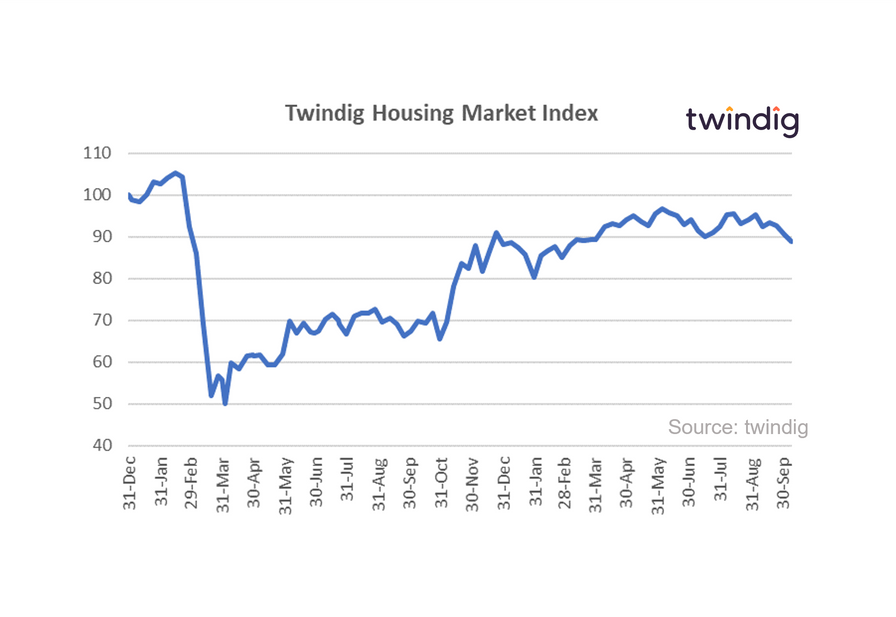

Twindig Housing Market Index

Boris's bullish building back rhetoric could not turn the tide on the Twindig Housing Market Index, which fell for a third week in a row this week. Investors did not share the Prime Minister's confidence that he could solve the national productivity puzzle, by fixing the broken housing market. Many believed that a high wage high skill economy would push house prices up further still, widening the affordability gap rather than narrowing it.

Away from the party conference opinions, the housing market facts were more promising. House prices reaching record highs in September according to the Halifax House Price Index as the stamp duty holiday came to close and mortgage rates, as reported by the Bank of England, continue to fall.