Houselungo 6 February 22

What does levelling up mean for homeownership?

On Wednesday, 2 February 2022, the Department for Levelling Up, Housing and Communities published its ‘Levelling Up the United Kingdom White Paper, a bold plan to unleash opportunity and create a more equal society. In this article, we look, specifically, at What levelling up means for homeownership.

Levelling Up – the rallying call for homeownership

“By 2030, renters will have a secure path to ownership with the number of first-time buyers increasing in all areas; and the government’s ambition is for the number of non-decent rented homes to have fallen by 50%, with the biggest improvements in the lowest performing areas.”

Source: Levelling Up the United Kingdom White Paper Executive Summary

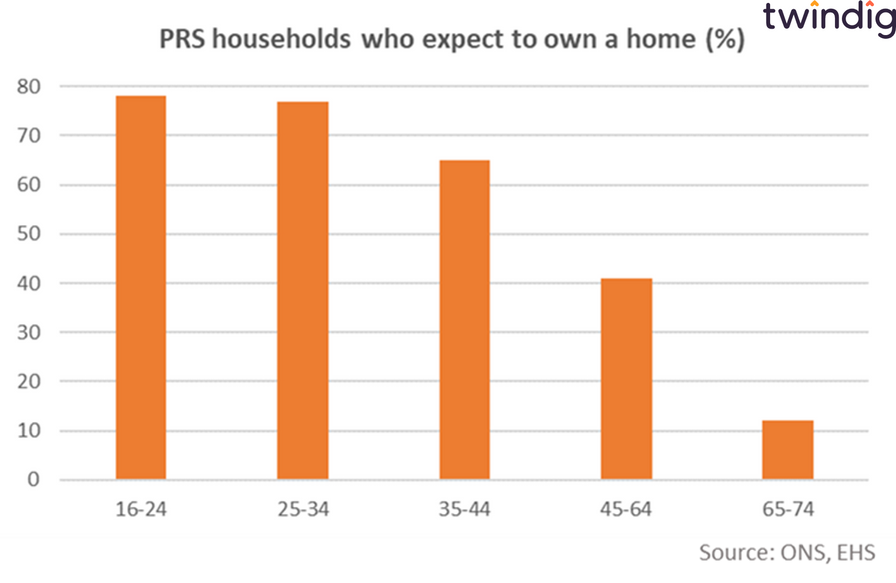

Most of us aspire to own our homes, especially those in rented accommodation as illustrated in the chart below, Brexit and COVID-19 and indeed rising house prices have done little to dent our enthusiasm or desire to own our homes.

The Levelling UP White Paper went on to say:

"We will ensure homeownership is within the reach of many more people. The Help to Buy scheme launched last year is focussing entirely on first-time buyers and we will build on the success of the Mortgage Guarantee Scheme by working with the lending industry to maximise the availability of low deposit mortgages."

We welcome the news that the Government will ensure that homeownership is within reach of many more people, but we don’t think that the existing policies, on their own, will deliver the desired results.

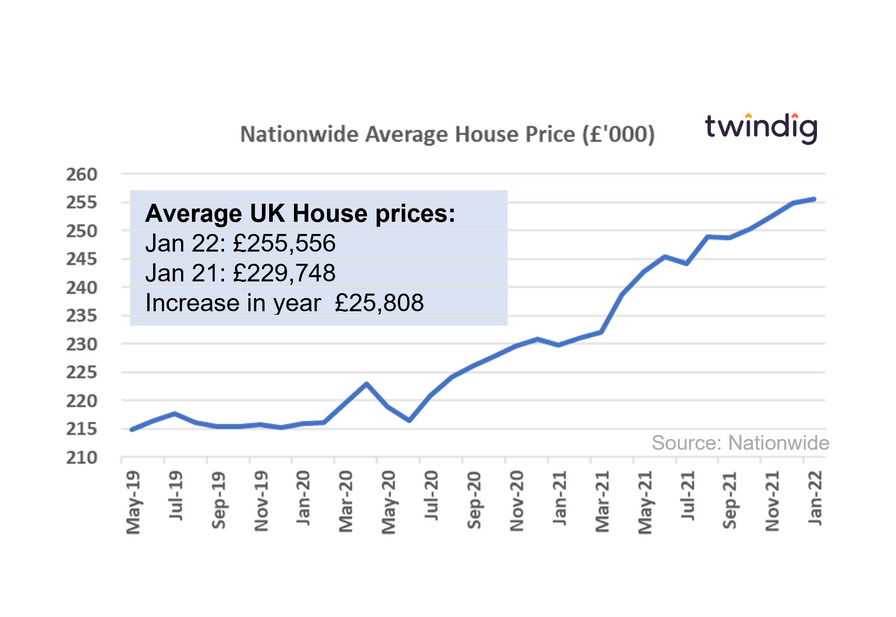

House prices rise by almost £500 per week

The Nationwide published their house price index for January 2022 this week

What they said

Average UK house prices £255,556

House prices increased by 11.2% or £25,808 over the last year

The strongest start to the year since 2005

Twindig take

House prices have had a strong start to 2022, in fact, the strongest start to a year for 17 years. Over the last year UK house prices increased, on average by almost £500 per week, but the Nationwide suggests that there are headwinds on the horizon.

Nationwide believes that the housing market will slow this year for a number of factors:

House price growth has significantly outstripped earnings growth since the start of the pandemic.

The anticipated cost of living increases this year, which will stretch the already stretched housing affordability metrics

Mortgage rates are also likely to rise this year as we expect that the Bank of England raise Bank Rate this year as it tries to control inflation.

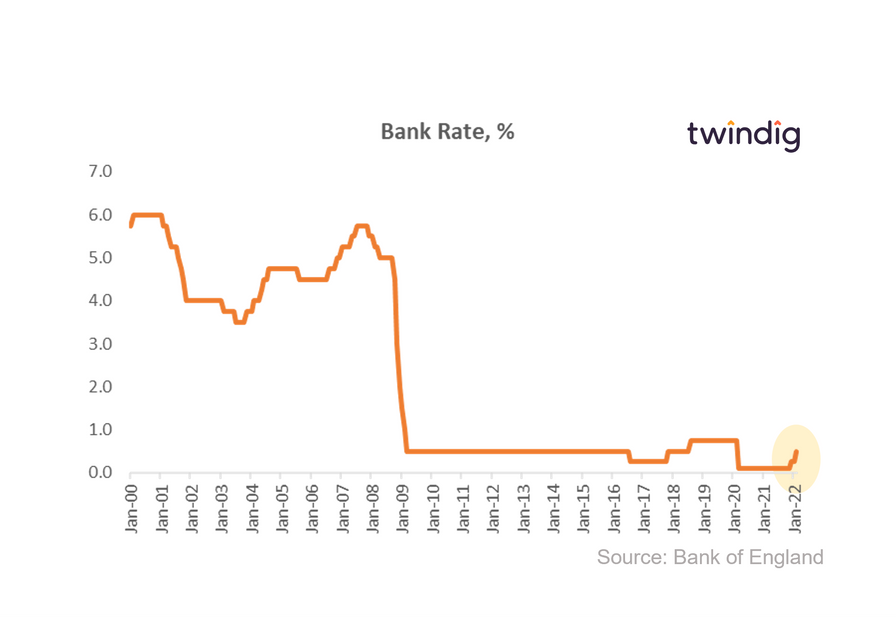

Bank Rate Doubles

The Bank of England voted 5-4 in favour of doubling the Bank Rate to 0.5% this week and we should expect more increases to come.

With inflation at record levels and expected to rise further it is no surprise that the MPC voted to increase Bank Rate today and the doubling to 0.5% is certainly worthy of grabbing a few headlines if there are any left to grab after the energy price hike stories fill the column inches.

However, the vote to double was a close run thing 5-4 in favour, although those in the minority had voted for a 0.5% rise to 0.75% a rise of 200%.

The prospect of further Bank Rate rises are therefore a racing certainty, in our view as the Bank of England looks to curb the rise of inflation, which it expects to increase further in coming months, from 5.4% to close to 6% in February and March, before peaking at around 7¼% in April.

It is certainly unfortunate timing to announce the rise in Bank rate on the same day as households received the hammer blow of energy price increases and will squeeze further already squeezed costs of living.

However, there may be a grey, if not silver,lining to the cost rising cloud.

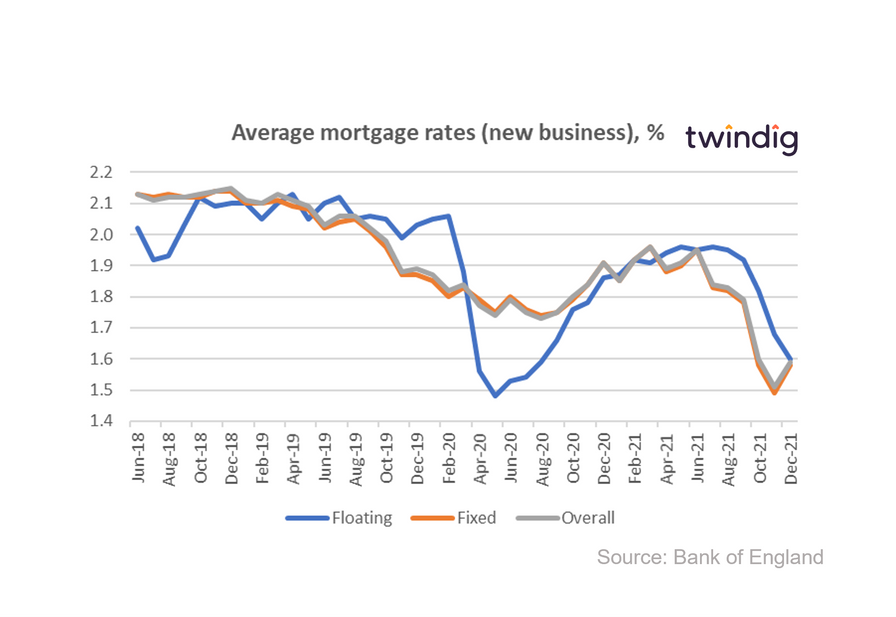

Average mortgage rates on the turn

The latest data from the Bank of England reveals that after months of falls, average mortgage rates for new business started to rise in December 2021.

What they said

The average floating mortgage rate for new business 1.60%

The average fixed mortgage rate for new business 1.58%

The average overall mortgage rate for new business 1.59%

Twindig Take

The Bank of England raised Bank Rate in December from its all-time low of 0.1% to 0.25% in part as a response to rising consumer price inflation. It is perhaps a surprise therefore that on new business, floating mortgage rates (which are typically linked to Bank Rate) actually fell.

It was not a surprise that fixed rates rose as lenders need to consider their funding costs over the fixed-rate period and the trends in loan pricing. Most commentators including ourselves expect Bank Rate to rise further in 2022 and we, therefore, believe lenders are factoring in the impact of future rate rises.

Twindig Housing Market Index

As the UK Government launched its White Paper explaining how it would seek to level up the UK economy, the Twindig Housing Market Index nudged up by 0.8% to 86.2.

We were surprised that housing market investors did not react more strongly to the news that energy prices will increase significantly, a story that appeared to us to garner more headlines than the Levelling Up White Paper and the doubling of Bank Rate seemed to pass without comment.

Significantly rising energy prices will impact households ability to save for a deposit and the reduction in disposable income will trim a homebuyers mortgage capacity, which, in theory, should impact house prices.

The doubling of Bank Rate, albeit from a very low base, will feed into mortgage costs and most, including ourselves, expect several more rate rises before the year is out.

Perhaps both stories highlight the fact that we live in an economy that needs levelling up. Some can participate in the housing market, whilst others can't and the impact of rising energy bills and interest rates does not appear to negatively impact those who can.