Houselungo 19 September 21

A lungo length look at this week's housing market news

House prices fall as Stamp Duty benefit is cut

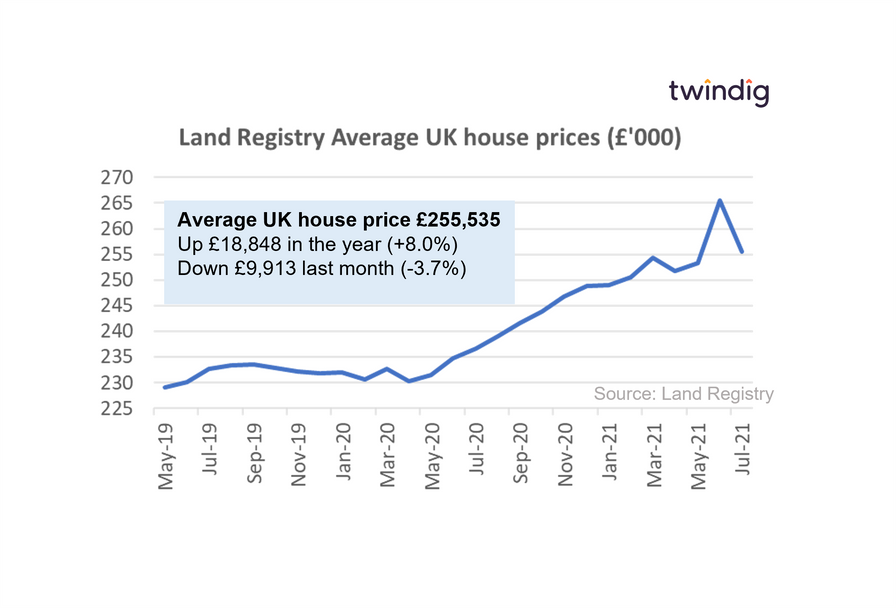

The Land Registry released its latest house price data for July 2021 today

What they said

Average UK house prices in July £255,535

An increase of +8.0% or £18,848 in the year

A fall of -3.7% or £9,913 in the month

Twindig take

According to the latest data from the Land Registry, average UK house prices fell by almost £10,000 in July, the first month following the reduction in Stamp Duty Holiday benefit. However, on average house prices are almost £19,000 higher than they were one year ago.

UK House prices: A case of what goes up must come down?

The average house price in the UK is £255,535, average prices have increased by 8.0% or (£18,848) over the last year, and decreased by 8.0% or (£9,913) last month. We note that these figures are provisional and subject to change, however, the size and the scale of these increases reflects a reduction in housing market activity following the first of two reductions in the Stamp Duty Holiday benefit threshold. The Stamp Duty Holiday benefit level reduced from £500,000 on the 30 June 2021 to £250,000 from 1 July 2021 and the stamp duty holiday will come to an end on 30 September 2021.

UK average house prices have increased by 15.2% (£35,059) since the start of the COVID-19 pandemic.

UK house prices fell across all regions in July 2021, falling on average by £9,913 following the first of two stamp duty holiday deadlines.

Whilst significant, the price falls in July are subject to change and in our view reflect a short term adjustment following a period of very high stamp duty related housing market activity. In the medium term we expect demand to underpin house prices as homes for sale remain in short supply, in our view.

London house prices half up, half down

The latest data from the Land Registry shows that the average house price in London fell by 2.0% or £10,000 to £494,673 in July 2021. House prices fell in 17 of the 34 London boroughs.

The biggest London house price gains last month were to be found in Kensington and Chelsea up £102,995 or 8.4%, Hammersmith & Fulham up £59,138 or 7.9% and Hackney up £41,501 or 2.9%.

The biggest falls were in the City of London down 12.0% or £96,142, followed by Lambeth down £36,430 or 6.7% and Hounslow down £23,612 or 5.4%.

House Prices in London

The average house price in London is £494,673. This is 83% or £223,699 higher than the £270,973 average house price in England.

House prices in London have risen by 2.2% over the last twelve months compared to an average increase in house prices across England of 7.0%. In absolute monetary terms, this translates to an average increase of £10,843 in London and £17,747 in England. House prices in England have therefore increased more in both relative and absolute terms than they have in London over the last 12 months.

To see the house prices and house price trends by London borough keep reading, you will find all that house price data in the body of this article.

London House Price Outlook

In the short term, following the hiatus of the step change in the stamp duty holiday threshold, we expect house prices in London to increase. The move in house prices in July this year is similar to the pattern we saw in earlier in the year in April 2021 where house prices fell back as homebuyers agreed prices assuming that they would miss the original stamp duty holiday deadline of 31 March 2021. Once the stamp duty holiday impact has unwound, we expect London house prices to move up.

In the medium term as the pandemic, risks subside and the UK economy is re-opened we would expect to see a continued recovery in housing transaction volumes and positive momentum maintained for house prices.

Energy, Efficiency, and house price inequality

The climate is a changing

We increasingly live in a world where how we live is causing our climate to change and our weather to become ever more extreme. Climate change was one of the factors recited by my insurance company as they once again raised my home insurance premium – ‘Increased flash flooding and increased subsidence caused by climate change’.

One way to help combat climate change at a global level and your wallet at a local level is to make your home more energy-efficient, a kind of save your money and save the planet win-win.

Our boilers heat the planet as well as our homes

Nationwide recently published a Special Report looking into EPC ratings and house prices. Andrew Harvey, Nationwide’s Senior Economist reported in that “Decarbonising and adapting the UK’s housing stock is critical if the UK is to meet its 2050 emissions targets, especially given that the housing stock accounts for around 15% of the UK’s total carbon emissions.”

It would seem logical therefore that in these climate enlightened times, that homes with better Energy Performance Certificate) EPC rating should achieve better prices when sold.

Do lower carbon homes attract higher prices?

This is the $64 million question, Nationwide crunched the numbers so we don't have to, click read more below to find out...

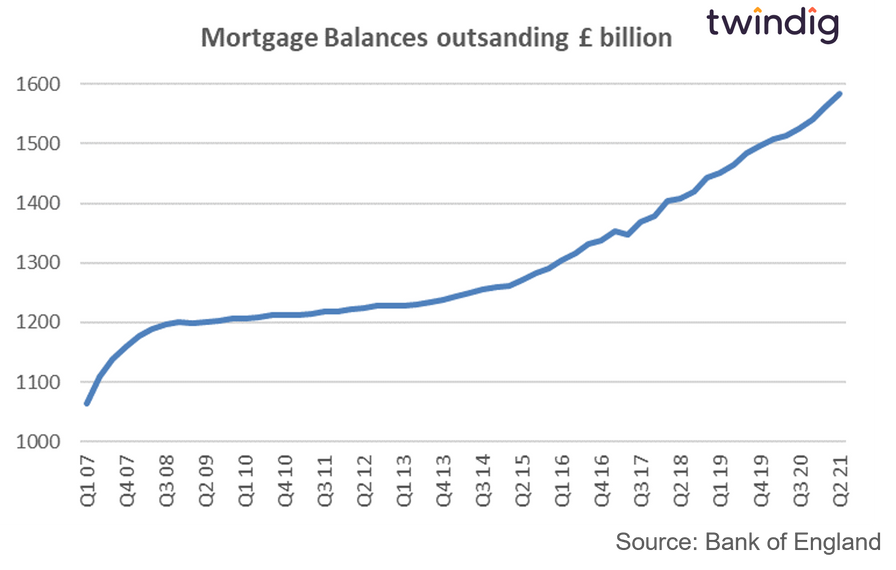

Mortgage Market Snapshot

Whilst not the most riveting read, this week’s ‘Mortgage Lenders and Administrators Return MLAR’ a statistical quarterly release on mortgage lending did include some interesting insights into the mortgage market and the housing market it serves (well perhaps only if you are a numbers geek..).

Despite mortgages being one of our biggest monthly outgoings, the UK mortgage market is surprisingly smaller than you think.

How big is the UK mortgage market?

The value of outstanding residential mortgage loans in the UK was £1,584 billion at the end of 2021. The value of mortgages outstanding has grown almost continuously since 2007. Growth paused for breath during the credit crunch and tripped over early Brexit concerns, before returning to a strong growth trajectory.

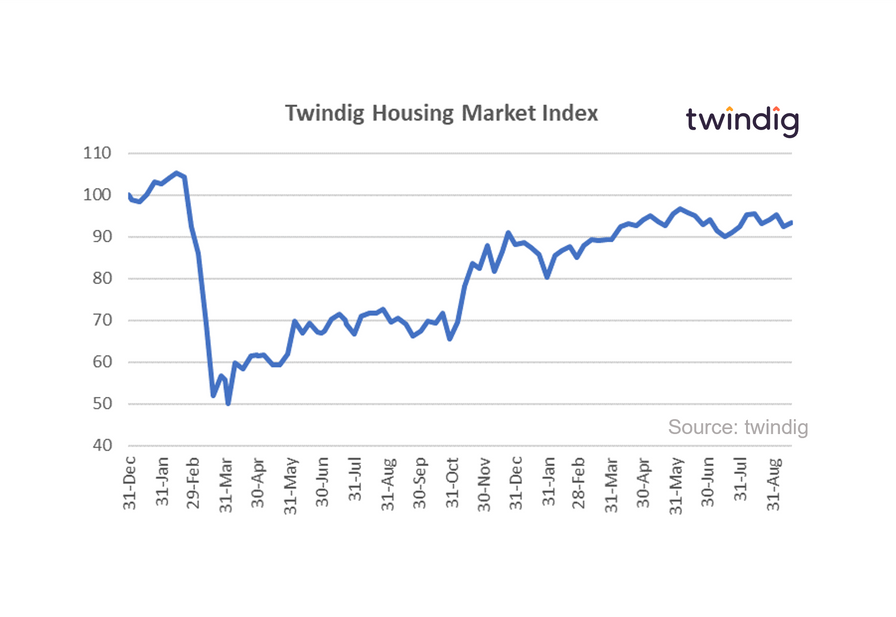

Twindig Housing Market Index

The Twindig Housing Market Index rose by 1.0% to 93.3 this week. Strong performance and bulging forward orderbooks reported by housebuilder Redrow this week and continued competition in the mortgage market led to an increase in investor confidence in the UK housing market. Confidence did, however, reduce in the estate agency due to concerns that continued stock shortages today may impact financial results tomorrow, although many were mindful that the shortages in homes for sale continue to underpin house prices. We also suspect that Michael Gove, the new housing minister will have a vested interest in seeing higher rather than lower house prices.